Preparing for a 340B compliance audit means ensuring that a covered entity fully complies with federal 340B Drug Pricing Program requirements, avoids diversion and duplicate discounts, and maintains accurate documentation to withstand audits by HRSA, manufacturers, or state regulators using 340B compliance services.

In 2026, compliance matters more than ever because audits are increasing, regulations are tightening, and financial penalties for non-compliance can be severe.

This guide explains what a 340B audit is, why it happens, what auditors look for, common red flags, and best practices for audit readiness, so healthcare organizations can stay compliant, protect revenue, and maintain program eligibility.

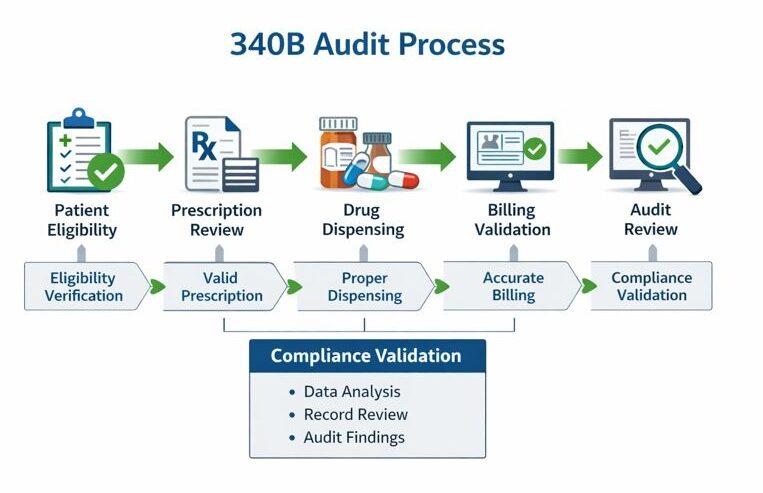

What Is a 340B Compliance Audit?

A 340B compliance audit is a formal review conducted to verify that a covered entity is following all rules of the 340B Drug Pricing Program.

Audits assess whether discounted 340B drugs are used only for eligible patients, billed correctly, and protected from duplicate Medicaid discounts.

Who conducts 340B audits?

Audits may be conducted by:

- HRSA (Health Resources and Services Administration)

- Drug manufacturers

- State Medicaid agencies

- Third-party auditors engaged by manufacturers

Each audit type has different triggers, scopes, and enforcement authority, but all focus on the same compliance fundamentals.

Why Are 340B Audits Increasing in 2026?

340B audits are increasing because of program growth, regulatory scrutiny, and financial risk tied to discounted drug pricing.

Key reasons audits are intensifying include:

- Expansion of contract pharmacy arrangements

- Increased manufacturer oversight and disputes

- Higher drug costs.

- Data transparency requirements

- Congressional and CMS scrutiny of 340B savings usage

In 2026, auditors rely more heavily on data analytics, making manual compliance processes riskier than ever.

What Are the Core 340B Compliance Requirements?

340B compliance is built on three non-negotiable pillars. Violating any of them can trigger audit findings.

1. What is diversion under the 340B program?

Diversion occurs when a 340B drug is dispensed to a non-eligible patient.

To avoid diversion, covered entities must ensure:

- The patient meets the HRSA 340B patient definition

- The provider relationship is documented

- The service occurs at a registered location

- Prescriptions align with eligible encounters

Even unintentional diversion can result in repayment and corrective action plans.

2. What is a Duplicate Discount in 340B?

A duplicate discount occurs when a manufacturer provides a 340B discounted drug and that same drug is also claimed through Medicaid in a way that is not properly identified as 340B, leading to an unintended overlap in discounts.

To prevent duplicate discounts, covered entities must:

- Correctly manage Medicaid billing by clearly defining carve-in or carve-out status

- Maintain accurate and up-to-date Medicaid billing identifiers

- Coordinate closely with state Medicaid agencies to ensure proper claim handling

Duplicate discounts are among the most common findings in 340B audits, making proper claim management and documentation critical for compliance.

3. Why is accurate recordkeeping critical for 340B compliance?

Auditors rely heavily on documentation.

Required records include:

- Patient eligibility documentation

- Prescriber credentials

- Claim-level transaction data

- Inventory reconciliation reports

- Medicaid billing flags

- Contract pharmacy agreements

Missing or inconsistent documentation is often treated as non-compliance, even if the entity followed the rules.

What Triggers a 340B Compliance Audit?

Audits are often triggered by patterns, not single mistakes.

Common audit triggers include:

- Unusual purchasing volumes

- Inconsistent Medicaid billing

- High contract pharmacy utilization

- Data mismatches between systems

- Prior audit findings

- Manufacturer dispute claims

Many organizations are audited without prior warning, making proactive readiness essential.

What Do 340B Auditors Review During an Audit?

Auditors follow a structured review process focused on data accuracy, eligibility, and controls.

What data do auditors request?

Auditors typically request:

- Prescription claims data (12–24 months)

- Patient encounter records

- Provider employment contracts

- Medicaid billing reports

- Inventory management logs

- Contract pharmacy files

They often test random samples and high-risk claims identified through analytics.

What systems are reviewed in a 340B audit?

Audits commonly examine:

| System | Purpose |

| EHR | Patient eligibility verification |

| Pharmacy system | Dispensing records |

| Claims processing | Billing accuracy |

| Split-billing software | 340B vs non-340B classification |

| TPA platforms | Contract pharmacy oversight |

Disconnected or manual systems increase audit risk.

What Are the Most Common 340B Audit Red Flags?

Understanding red flags helps organizations correct issues before auditors find them.

1. Why is patient eligibility the top red flag?

Incorrect patient eligibility is the number one audit finding.

Common issues include:

- Missing provider relationship documentation

- Prescriptions written outside registered locations

- Telehealth encounters not properly documented

- Referral-only encounters counted as eligible

Eligibility rules must be consistently applied, not assumed.

2. How do contract pharmacies create audit risk?

Contract pharmacies expand access, but also risk.

Red flags include:

- Poor oversight of multiple contract pharmacies

- Inaccurate replenishment logic

- Duplicate dispensing across locations

- Missing contract documentation

Auditors often scrutinize contract pharmacy claims more aggressively.

3. Why is inventory management a compliance risk?

Improper inventory controls can lead to:

- Mixed 340B and GPO stock

- Inaccurate replenishment

- Retroactive claim adjustments without documentation

Virtual inventory systems must be validated and reconciled regularly.

4. How does Medicaid billing cause audit failures?

Medicaid errors are common because:

- Billing flags are outdated

- State rules change

- Managed Medicaid complicates identification

Even one incorrect Medicaid claim can result in a duplicate discount finding.

What Are Best Practices for 340B Audit Preparation in 2026?

Audit readiness is not a one-time task, it is an ongoing operational discipline.

1. How can organizations conduct internal mock audits?

Internal audits simulate real audit conditions.

Best practices include:

- Quarterly claim sampling

- Cross-functional reviews (pharmacy, IT, billing)

- Testing eligibility documentation

- Reviewing Medicaid carve-in/out logic

Mock audits identify issues early and reduce panic during real audits.

2. Why is automation essential for 340B compliance?

Manual processes increase error rates and audit exposure.

Automation benefits include:

- Real-time eligibility validation

- Automated duplicate discount detection

- Claim-level audit trails

- Centralized documentation storage

By 2026, auditors expect technology-enabled compliance, not spreadsheets.

3. How should covered entities manage contract pharmacy oversight?

Strong oversight includes:

- Regular performance reviews

- Clear data-sharing agreements

- Defined replenishment timelines

- Ongoing eligibility validation

Organizations should limit contract pharmacies to those they can actively monitor.

4. What role does staff training play in audit readiness?

Training prevents unintentional violations.

Key training areas:

- HRSA patient definition

- Medicaid billing rules

- Documentation standards

- Audit response protocols

Staff turnover without retraining is a hidden compliance risk.

How Should Organizations Respond When Notified of a 340B Audit?

A structured response protects outcomes.

Immediate steps include:

- Assign a single audit lead

- Secure legal or compliance counsel if needed

- Freeze relevant data sets

- Validate requested documentation

- Respond accurately, never guess

Clear communication and timely responses significantly influence audit results.

What Are the Consequences of 340B Non-Compliance?

Audit findings can have financial and operational consequences.

Possible outcomes include:

- Repayment to manufacturers

- Corrective action plans (CAPs)

- Loss of contract pharmacy privileges

- Program removal in severe cases

- Reputational damage

Proactive compliance costs far less than remediation.

How Does 340B Compliance Support Long-Term Sustainability?

Strong compliance enables:

- Stable program participation

- Financial predictability

- Manufacturer trust

- Reduced legal exposure

- Better patient access to care

Compliance is not just regulatory, it is strategic.

Real-World Example: A Hypothetical 340B Audit Scenario

A mid-size hospital with 12 contract pharmacies undergoes a manufacturer audit.

Findings include:

- Missing provider documentation for telehealth visits

- Incorrect Medicaid billing flags

- Delayed inventory reconciliations

Result:

- $1.2M repayment avoided by demonstrating corrective actions

- Implementation of automated compliance software

- Quarterly internal audits established

Lesson: Preparation changes outcomes.

Final Thoughts: Preparing for 340B Audits in 2026 and Beyond

Preparing for a 340B compliance audit in 2026 requires clarity, consistency, and control. As audits become more data-driven and enforcement more stringent, healthcare organizations must move from reactive compliance to proactive governance.

By understanding requirements, recognizing red flags, and adopting best practices, including automation and continuous monitoring, covered entities can protect their programs, finances, and mission to serve vulnerable populations.

Frequently Asked Questions (FAQ)

What is the most common reason for failing a 340B audit?

The most common reason is patient eligibility errors, especially missing documentation linking the prescriber, patient, and covered entity.

How often do 340B audits occur?

Audits can occur at any time. Some entities are audited every few years, while others may face multiple audits in a short period.

Can contract pharmacies be audited separately?

Yes. Manufacturers often audit contract pharmacy claims, and covered entities remain fully responsible for compliance.

Is 340B software required for compliance?

While not legally required, software is increasingly necessary in 2026 due to data complexity, audit expectations, and scale.

What should be done after an audit finding?

Organizations should implement corrective action plans, repay identified discrepancies if required, and strengthen controls to prevent recurrence.

How long should 340B records be retained?

Most organizations retain records for at least 5–7 years, depending on audit risk and state requirements.